Can’t Afford Your NYC Mortgage? The Homeowner’s Guide to Short Sales

The financial realities of 2026 are pushing many hardworking families in Brooklyn and Queens into a corner. Between inflation, shifting property tax assessments, and the rising cost of living, keeping up with a mortgage can suddenly become impossible.

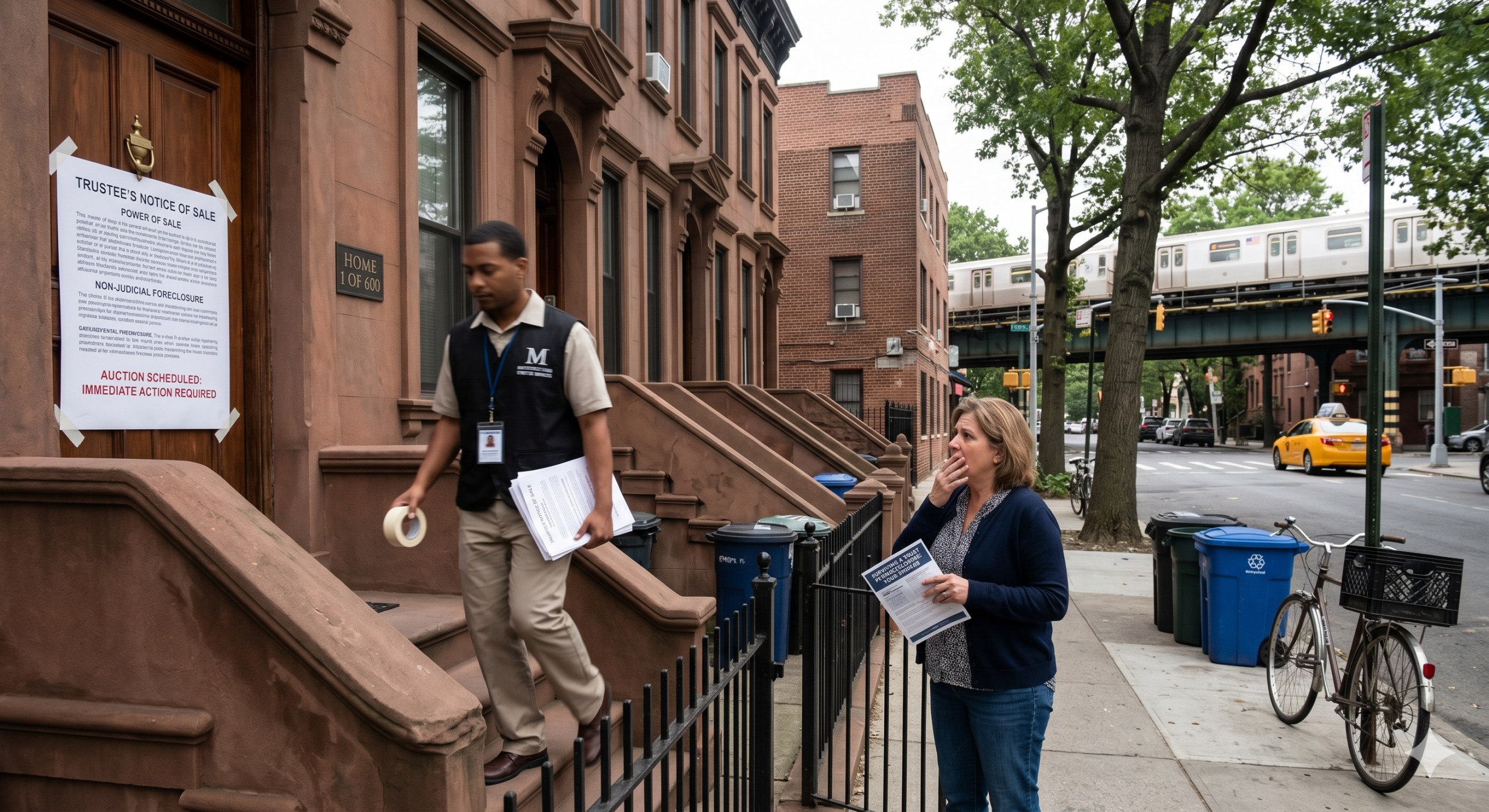

If you have fallen behind on your payments and realize that you owe the bank more than your property is currently worth, you are dealing with an “underwater” mortgage. When you are in this position, you cannot simply list the home and pay off the bank with the profits, because the market value won’t cover the total debt.

Feeling trapped leads many homeowners to freeze and simply wait for the foreclosure notice. But doing nothing is the most dangerous option. Here is why you need to act now, the legal traps to avoid, and how a short sale can offer you a clean slate.

The Ticking Clock: Federal Assistance is Drying Up

If you have been relying on federal or state grace periods to keep the bank at bay, that window is rapidly closing. The Homeowner Assistance Fund (HAF)—a federal program established to help homeowners financially impacted by COVID-19 with housing-related costs—is officially scheduled to end in September 2026, or as soon as the remaining funds have been used up. As these safety nets disappear, lenders are accelerating their collection and foreclosure efforts across the five boroughs.

The Danger of the “Quick Fix” Loan Modification

When facing foreclosure, many homeowners desperately try to secure a loan modification to lower their monthly payments. While this can sometimes be a valid strategy, it carries massive hidden risks in 2026.

A recent New York Appellate Division ruling (Ditech Financial LLC v Temple) serves as a stark warning to distressed homeowners: if you agree to modify your mortgage note after the six-year statute of limitations on a foreclosure has expired, you can actually revive your lender’s right to foreclose against you. Signing the wrong paperwork without legal or professional guidance can instantly reset the clock in the bank’s favor, stripping you of your leverage.

What is a Short Sale?

If a loan modification isn’t viable and you cannot afford the home, your best exit strategy is often a short sale.

A short sale occurs when you successfully negotiate with your mortgage lender to sell the home for less than the outstanding balance of the loan. In exchange for you facilitating the sale and handing over the proceeds, the bank agrees to release the mortgage lien, allowing the sale to go through.

Why a Short Sale is Better Than Foreclosure

Convincing a bank to take a loss requires heavy negotiation and mountains of paperwork, but the benefits for the homeowner are undeniable:

- Save Your Credit Score: A finalized foreclosure stays on your public record and destroys your credit score for seven years, making it nearly impossible to rent a decent apartment or buy another home. A short sale avoids a foreclosure hitting your credit report, doing significantly less damage and allowing you to recover much faster.

- Control Your Timeline: If you wait for the bank to foreclose, a judge will eventually order an auction, and a sheriff will enforce an eviction. A short sale allows you to move on your own timeline, not a bank’s. You leave the home on your terms, with your dignity intact.

- Avoid Deficiency Judgments: In many short sale negotiations, a skilled real estate broker can get the bank to waive their right to a “deficiency judgment,” meaning they legally agree not to come after you later for the remaining unpaid balance.

You Need an Expert Negotiator

Banks do not make short sales easy. They require a mountain of evidence proving your financial hardship, and they need a fully vetted buyer ready to close.

At the LJ Realty Team, we have over 21 years of experience navigating the complexities of the Brooklyn and Queens real estate markets. We know exactly how to speak to the banks, how to package your hardship application, and how to find cash buyers willing to navigate the short sale process.

Do not wait for the bank to make the first move. Contact Sheldon The Realtor online today for a fully confidential consultation on whether a short sale is the right strategy for you.