The 2026 NYC Tax Lien Sale is Paused: What Mayor Mamdani’s Decision Means for Your Property Debt

If you own a home in Brooklyn or Queens and have fallen behind on your property taxes, water and sewer bills, or municipal repair charges, you are likely familiar with the sheer anxiety of the annual NYC tax lien sale.

Historically, when property owners failed to resolve these debts, the city would package the debt and sell it to a third-party, private entity known as the Tax Lien Trust. Once the Trust owned your debt, the situation escalated rapidly. They would tack on heavy administrative costs and aggressively compound the interest—charging 9% per year for homes assessed between $250,000 and $450,000, and a staggering 16% per year for homes assessed over $450,000. If left unpaid, the Trust had the power to foreclose on your home and auction it off.

But 2026 has brought a monumental shift to how New York City handles property debt. Here is exactly what the recent legislative changes mean for you, and why you cannot afford to simply ignore your past-due bills.

The Big News: The 2026 Lien Sale is Paused

After years of intense pushback from housing advocates who argued the lien sale disproportionately harmed Black and Hispanic communities and stripped generational wealth from outer-borough families, the system is finally changing.

In January 2026, the City Council overrode a mayoral veto of a bill package designed to abolish the lien sale as we know it. Following this legislative momentum, Mayor Zohran Mamdani officially announced in March 2026 that there will be no 2026 lien sale.

The administration is using this critical pause to review the entire debt collection program and consider enacting alternatives that do not rely on selling resident debt to private, profit-driven investors.

What is the Alternative? The Community Land Bank

Instead of feeding struggling homeowners to a private trust, the City Council is actively pushing to replace the lien sale with a publicly-accountable land bank.

What does this mean for you? If established, this land bank would take over the outstanding municipal debts. However, rather than aggressively pushing for foreclosure and displacement, the land bank’s primary mandate would be keeping people in their homes, preserving homeowners’ hard-earned equity, and supporting affordable housing under community control.

While the exact mechanics of how homeowners will interact with this new land bank are still being finalized for the Fiscal Year 2027 budget, the overarching goal is preservation rather than punishment.

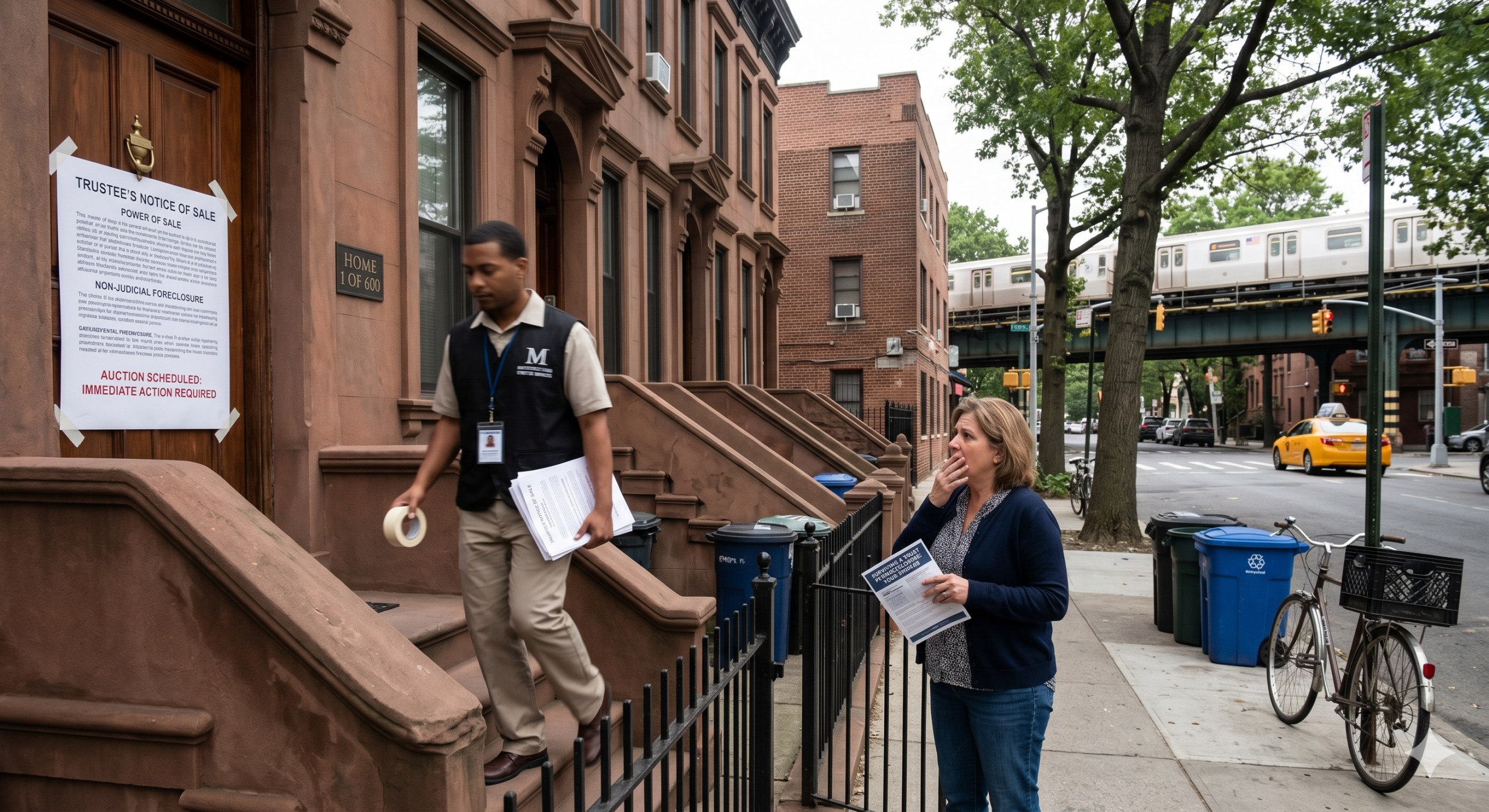

Warning: If Your Debt Was Already Sold, You Are Still at Risk

While the pause on the 2026 sale is a massive relief for homeowners who recently fell behind, it does not erase the past.

If your tax or water debt was sold to the Tax Lien Trust in a previous year (such as during the 2025 sale), that private entity still owns your debt and is still actively pursuing collection. In fact, according to recent data, there are currently nearly 600 one-to-three-family homes actively trapped in the lien foreclosure process initiated by the Trust.

If you have received notices from the Tax Lien Trust regarding past sales, your home is still in imminent danger of being auctioned. The 2026 pause does not stop existing Trust foreclosures from moving forward.

How to Use This “Breathing Room” to Protect Your Equity

If you are behind on your taxes but your debt has not been sold, you have been given a golden opportunity. Do not waste this pause. The city will eventually collect what is owed, and letting your property taxes compound will slowly eat away at the equity you hold in your property.

Here are your best strategic moves right now:

- Establish a Payment Plan: Reach out to the Department of Finance immediately to set up a standard payment agreement (SPA). This protects your property from future enforcement actions as long as you make your agreed-upon monthly payments.

- Evaluate Your Financial Reality: If the combined weight of your mortgage, rising insurance premiums, and back taxes is simply too much to bear, keeping the property might be a losing financial battle.

- Consider a Strategic Sale: Selling your property on the open market allows you to use the proceeds to pay off the city in full, satisfy your mortgage, and walk away with your remaining equity in cash. If the home is distressed or you need to sell before a past Trust foreclosure catches up to you, taking a fast, “as-is” cash offer can bypass the traditional market entirely and get you out of debt in less than 30 days.

Get Expert Guidance Today

Navigating the shifting landscape of NYC property taxes requires a local expert who intimately understands the Brooklyn and Queens markets.